The Overlooked Customer Nobody Built For

The following article is offered for informational purposes only, and is not intended to provide, and should not be relied on, for legal or financial advice. Please consult your own legal or accounting advisors if you have questions on this topic.

There's a customer that every fintech company ignores. Not because they're small or unprofitable. Because they're hard to see. And even harder to truly understand.

I'm talking about the super premium, closely held business owner. The person who generates somewhere between $3 million and $100 million in revenue. Who owns two, three, maybe six businesses across different entity types. Who has a trust, a personal portfolio, a few properties, maybe a fund, and a household that runs more like a small operation than a family budget.

This person is not small business. They’re also not traditional mid-market. They're past the Stripe Atlas stage. They have real revenue, real employees, real complexity. But they're also not enterprise. They don't have a 50-person finance team. They might have a bookkeeper, an outside accountant, and a wealth advisor who doesn't talk to either of them. They typically have an amazing gal or guy who holds everything together.

Fintech has built extensively for both ends of this spectrum. There are hundreds of amazing unbundled products for small business and startups. And there are massive platforms (SAP, Oracle, Workday, Ramp, Brex) for enterprise. The closely held business owner sits somewhere adjacent to the middle, and nobody has built for them specifically.

Why This Customer Is Different

The closely held business owner has a set of characteristics that make them fundamentally different from both small business and enterprise customers.

Their business and personal finances are inseparable. Not because they're sloppy. Because that's how ownership works. The owner takes distributions. They personally guarantee business debt. They reimburse themselves. Their household expenses cross entity lines. Their wealth advisor needs to see the business cash position. Their accountant needs to see personal transactions that affect business taxes. The boundary between "business" and "personal" is a legal requirement but the actual experience for that owner is very different.

They operate across multiple entities. They may not think of themselves as multi-entity but they almost always have more than one. A typical Flex customer might have an operating company, a holding company, a real estate LLC, and a trust. Each entity has its own bank accounts, credit relationships, vendor contracts, and compliance requirements. No financial product understands that these entities are all part of one owner's world.

They don't have a finance team. The enterprise customer has an office of the CFO, a controller, an AP clerk, a treasury analyst. The closely held business owner has themselves, someone that keeps things going, maybe a part-time bookkeeper, and a CPA they talk to quarterly. Maybe two CPAs that don’t talk to each other between business and personal. The operational burden of managing complex finances falls on the owner directly, or it falls through the cracks.

They are usually naive about what's possible. Not because they're unsophisticated. Because nobody has ever shown them a better way. They've been cobbling together point solutions for so long that they think the friction is normal. They think month-end close should take three weeks. They think reconciling across entities requires a spreadsheet. They think managing five bank relationships is just part of being successful. Our customers are often not even asking for help because they’re resilient. And they’re just used to it at this point.

It doesn't have to be this way.

Why Fintech Ignores Them

Fintech companies build for addressable markets that are easy to define. Small business is easy to define. Enterprise is easy to define. Typical mid-market is easy to define. The closely held business owner is hard to define because they look different from each other.

A restaurant group owner with 12 locations looks nothing like a real estate investor with a portfolio of LLCs. A construction company owner with a bonding requirement looks nothing like a medical practice owner with multiple partners. But they all share the same structural problem: complex, multi-entity financial lives with no integrated infrastructure to manage them. And fruitful personal lives as the result of their hard work and success.

The other reason fintech ignores this customer: solving their problem is hard. You can't serve them with a single product. Expense management alone doesn't do it. Banking alone doesn't do it. Credit alone doesn't do it. You need the whole stack, and you need it to be connected. That's an enormous investment in infrastructure before you can deliver the experience that actually matters.

Most fintech companies are optimized to build one product, scale it fast, and monetize transactions. The closely held business owner needs something different. They need a platform that understands their entire financial picture and coordinates across it.

What These Owners Actually Need

When I talk to business owners, they don't describe their problem in product terms. They don't say "I need better expense management" or "I need a new bank." They describe symptoms.

"I spend all my time on stuff that should be easy."

“I don’t care enough about this.”

"My accountant and I are never on the same page and it’s a constant game of catch up."

"I have no idea how much cash I actually have across everything."

"I'm scared to buy another business because I can't handle the complexity I already have."

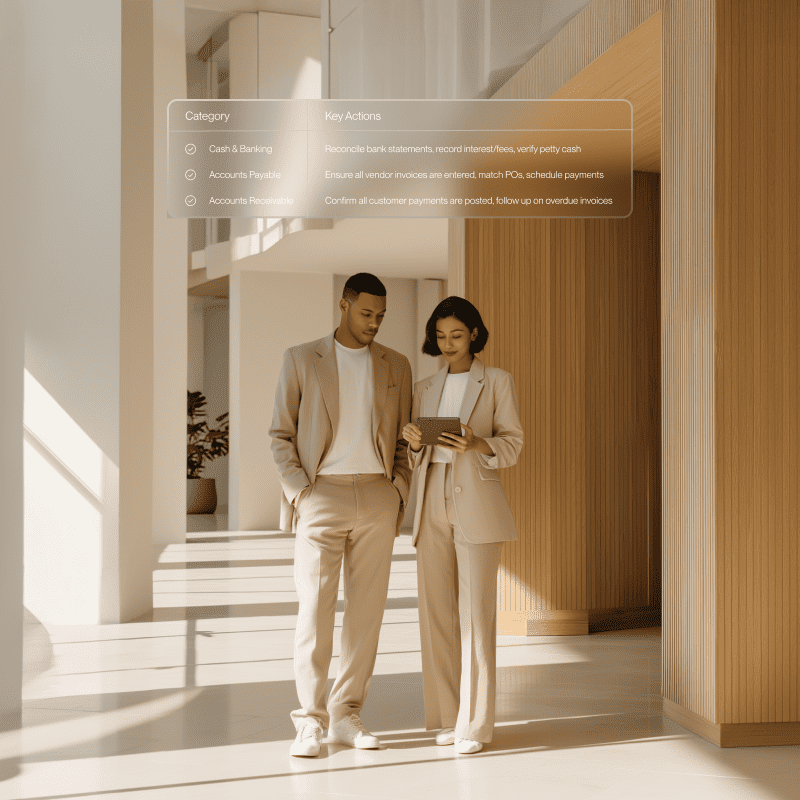

What they need is not a product. It's a system that removes the operational burden of managing complex finances. Built specifically for them. Something that understands their entities, their relationships, their policies, and their goals. Something that coordinates banking, credit, payments, bill pay, expense management, and lending into a single experience that reflects how they actually operate. Because they should be focused instead on building their businesses.

That's what we're building at Flex. Not for small business. Not for enterprise. For the owner on the side that nobody built for.

Why Now

Two things make this possible today that didn't exist five years ago.

First, the infrastructure primitives in fintech have matured. Issuing cards, moving money, managing ledgers, underwriting credit. The building blocks are available. What's missing is someone willing to assemble them into a coherent system for this specific customer. A great “rebundling” is occurring (with a number of other great providers as well). Simon Taylor at Fintech Brainfood wrote about this in a great “zoomed out” piece recently (check them out).

Second, AI has reached the point where coordination agents are practical. But only if they have the right data and infrastructure underneath them. An AI agent that can see an owner's full financial picture, apply their policies, and take action on their behalf requires a unified data model that spans every product. You can't bolt that on after the fact. You have to design for it from day one. And they must solve actual significant pain points for customers in addition to reducing friction slightly in day to day life.

The closely held business owner has been ignored long enough. They deserve financial infrastructure that's as sophisticated as their businesses. That's the gap. And it's the one we intend to close.

.png)

.svg)