GL Accounts: Everything Business Owners Should Know

The following article is offered for informational purposes only, and is not intended to provide, and should not be relied on, for legal or financial advice. Please consult your own legal or accounting advisors if you have questions on this topic.

Understanding your company’s financial health begins with knowing what’s happening in your general ledger (GL). This account is the foundation of your financial reporting system. It tracks every transaction, categorizing financial activity, and helping you maintain accurate records.

Having a strong grasp of how GL accounts work is essential to effective accounting and compliance. This guide will explain what a GL account is, how it functions in a GL ledger, the types of accounts you'll encounter, and how to manage them efficiently.

What Is a GL Account?

A GL account is a record used to classify and summarize financial transactions within a business. These accounts are part of the GL, which serves as the central repository of all financial activity.

Each time a transaction occurs — whether it’s a sale, expense, or bank transfer — it’s recorded in the general ledger and categorized into the appropriate GL account.

Key functions of a GL account:

- Track income, expenses, assets, and liabilities

- Support financial reporting and audits

- Organize data for tax and compliance purposes

- Provide visibility into business performance

How GL Accounts Work

Every GL account falls under a broader accounting category and is identified by a unique account number or code. These accounts are used in double-entry bookkeeping, where every transaction affects at least two accounts: one debit and one credit.

For example, if you purchase office supplies:

- Debit: Office Supplies Expense (increases expenses)

- Credit: Cash or Accounts Payable (reduces assets or creates liability)

These entries are posted to your GL ledger, ensuring your financial records remain balanced and traceable.

Types of GL Accounts

GL accounts are grouped into five core categories that reflect the structure of your balance sheet and income statement:

Each GL account typically has its own unique number for tracking and organization. For example:

- 1010: Cash

- 2010: Accounts Payable

- 4010: Sales Revenue

- 6010: Office Supplies

Examples of Common General Ledger Accounts

Here’s a quick look at real-world GL accounts small to mid-sized businesses commonly use:

How GL Ledgers Support Financial Reporting

The GL ledger consolidates all journal entries into organized account categories, creating the basis for your:

- Balance sheet

- Income statement

- Cash flow statement

This central structure allows finance teams to:

- Spot errors quickly

- Reconcile bank accounts

- Comply with audits

- Track performance by department or project

Best Practices for Managing GL Accounts

To keep your GL ledger clean and effective, consider these tips:

- Use a chart of accounts (COA): A standardized structure of GL accounts tailored to your business

- Close books monthly: Regularly review and reconcile your accounts to ensure accuracy

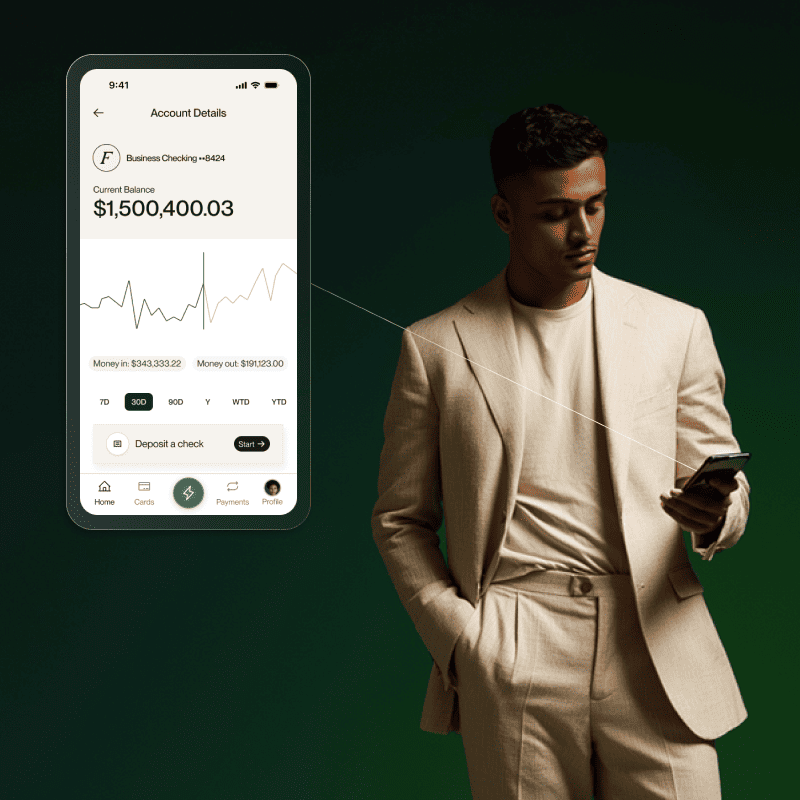

- Automate categorization: Use accounting software that integrates with expense tools like Flex for consistent GL coding

- Limit GL account sprawl: Avoid creating redundant or overly specific accounts that clutter reporting

- Monitor changes: Restrict permissions so only authorized staff can modify GL structures

Why GL Accounts Matter for Business Owners

Accurate and organized GL accounts give business owners critical visibility into:

- Profitability by department or product

- Cash flow trends

- Budget vs. actual spending

- Compliance risks or red flags

When your general ledger accounts are structured well, you can rely on your financial reports to drive better, faster decisions.

Final Thoughts

Your GL account system is the foundation of business finance. It's how you track the money moving in and out of your company. By understanding how general ledger accounts work — and setting them up effectively — you empower your business to scale with confidence.

Ready to streamline your GL process? Financial management tools like Flex can help ensure your spend is always correctly coded, categorized, and connected to your reporting.

.jpg)