Why Separating Business and Personal Finances Matters

The following article is offered for informational purposes only, and is not intended to provide, and should not be relied on, for legal or financial advice. Please consult your own legal or accounting advisors if you have questions on this topic.

Whether you're a business owner, startup founder, or a freelancer, separating business and personal finances is one of the most important — and often overlooked — foundations of long-term business success. While it may seem simpler to use one bank account for everything, doing so puts your business, your taxes, and even your personal assets at serious risk.

So why is keeping personal and business finances separate important? Here’s what every business owner needs to know — including legal, tax, operational, and financial credit reasons to keep these accounts separate. Leveraging individual accounts for your business and personal financial needs is the smartest decision you can make.

Why is it important to separate personal and business finances?

Separating business and personal finances is vital for a successful business – but why? Differentiating between the various financial aspects of your life not only helps you stay organized, but it can provide legal liability protection, establish a credit history specifically for your organization, simplify taxes, and more.

Legal Benefits

If you’ve registered your business as an LLC or corporation, you’ve taken the first step to protect your personal assets. But that protection only holds if you maintain a clear boundary between your business and personal finances.

Build legal credibility:

Courts and creditors look for clear financial separation when determining if your business is truly independent. If you mix your personal and business finances, it may appear like you’re just doing a hobby. But if you keep them separate, it shows you’re serious about running a real business, with legal structure and formal processes.

Preserve limited liability

If your business were to be sued or go into debt, your personal assets — like your home, savings, or car — will be protected. But if you mix your business and personal money, a court could decide you're not really treating your business as a separate entity. In that case, they could "pierce the corporate veil", which is a legal way of saying they may ignore your business protections and come after your personal assets to cover business debts. Keeping your finances separate helps prevent this from happening.

Demonstrate compliance

Having a dedicated account proves you’re managing your business money properly — which can help protect you. By using a separate business bank account, you're proving you’re handling your business money the right way. For example, if your business ever gets audited by the IRS or involved in a legal dispute, having a business account shows you’re doing things by the book.

Clean Tax Season

Mixing personal and business expenses can make filing your taxes particularly messy — and riskier. When your records are disorganized, you could miss deductions or trigger red flags with the IRS.

Tax benefits of separating business and personal finances:

- Easier to claim deductions and credits: You’ll have clean documentation for expenses like travel, supplies, or software subscriptions.

- Clean, audit-ready records: Should the IRS audit your business, you'll be able to provide clear, organized financials without digging through personal statements.

- Streamlined reporting: Accounting software can sync with your business account to automatically categorize and summarize business expenses.

Credit and Financing Opportunities

When your finances are separated, you can begin building a credit history for your business — an essential step for fostering growth and securing future funding.

- Establish creditworthiness: Business credit cards, loans, and trade lines can be reported to commercial credit bureaus, helping your business build a score.

- Qualify for loans: A solid business credit history can unlock lines of credit or financing that would otherwise require a personal guarantee.

- Reduce personal liability: With a strong business credit profile, you’re less likely to rely on your own credit or personal collateral for funding.

Operational Clarity and Cash Flow Management

Separate accounts can give you a real-time view of your business’ performance and can help you make smarter decisions.

Operational benefits include:

- Budgeting and forecasting: Know exactly what’s coming in and going out, without having to comb through and separate your personal transactions.

- Better decision-making: Clarity on revenue and expenses empowers you to make well-informed, financially smart decisions when planning for growth or adjusting when times are lean.

- Professional appearance: Clients and vendors may take you more seriously when you pay from a business account or receive ACH payments into a business-branded account.

How to Separate Business and Personal Finances

If you're serious about growing your business — or protecting your personal assets — separating your finances is more than just a best practice. It’s a smart move that gives you clarity, control, and credibility. The process is relatively straightforward and well worth the additional effort.

Here’s a step-by-step approach to help you draw the line between personal and business funds.

Separating Business and Personal Finances Step-by-Step

Step 1: Open a business bank account

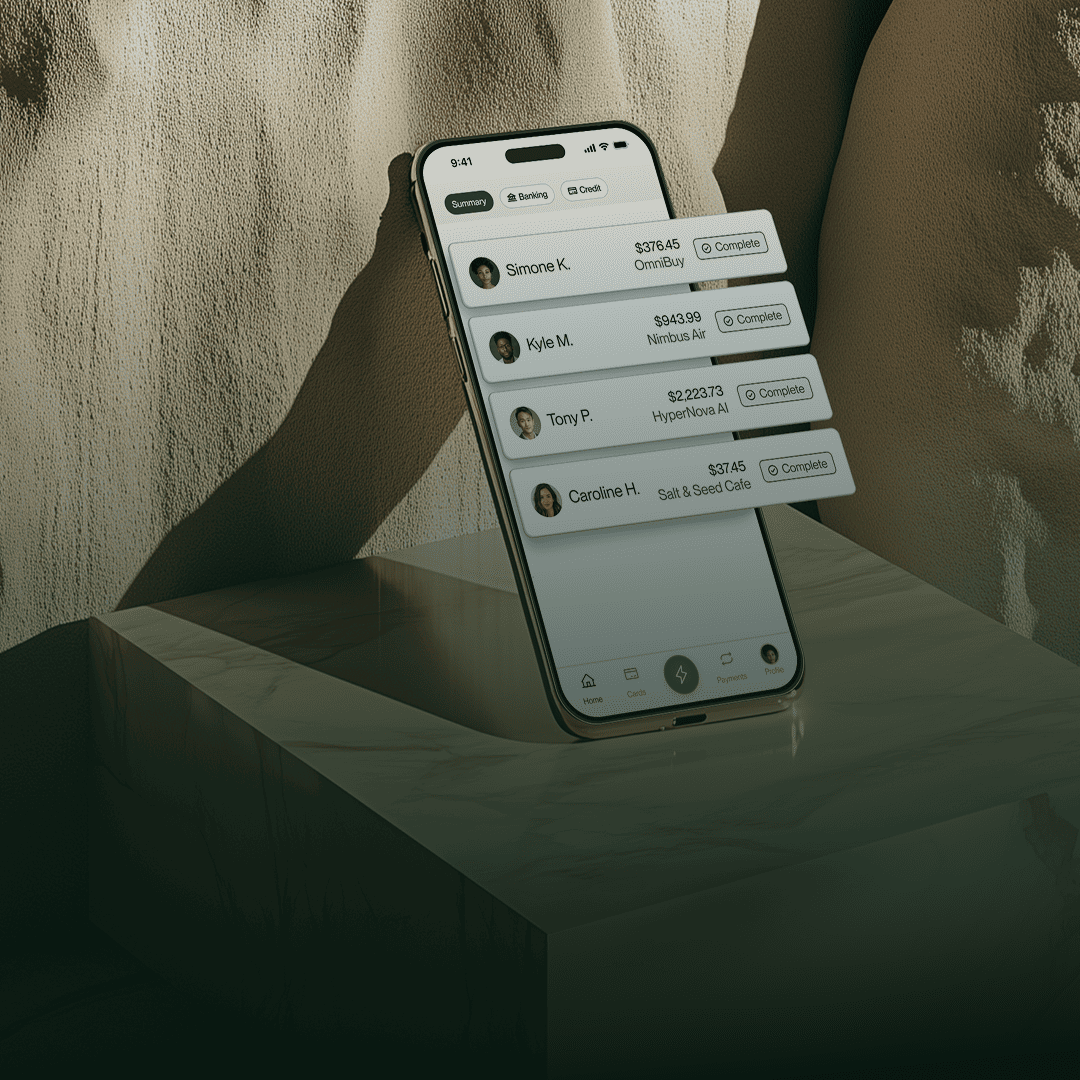

The first — and most critical — step is opening a dedicated business bank account. This ensures your company’s finances are legally and operationally distinct from your own.

Look for a business banking platform that makes this step seamless with:

- No hidden fees or monthly minimums — ideal for new and growing businesses

- Fast setup — get started online in minutes, without paperwork headaches

- Smart spend management — assign virtual or physical cards to team members, track transactions by category, and control spending in real time

- Cash flow forecasting tools — get a clear picture of what’s coming in and going out

- Built-in expense tracking — automatically organizes spending so you’re ready for tax season

Unlike traditional banks, Flex is built from the ground up to serve business owners, startups, and modern entrepreneurs. You’re not just opening an account — you’re gaining a command center for your business finances.

Step 2: Apply for a business credit card

Using a business credit card helps you keep all your operational spending — from software subscriptions to business travel — in one clean, trackable place.

The best cards give you:

- Customizable virtual and physical cards

- Spending limits by user, category, or vendor

- Real-time tracking of every charge

- Easy-to-export reports that integrate with your accounting software

Step 3: Pay yourself the right way

Don’t treat your business bank account like a piggy bank. To maintain clean books and legal protection you should pay yourself intentionally and consistently.

Depending on your business structure:

- Sole proprietors and single-member LLCs can take owner’s draws (regular transfers from your business account to a personal account).

- S-Corp owners should run payroll (Flex integrates easily with payroll platforms to simplify this).

Paying yourself this way ensures:

- Your books reflect accurate business profit

- You can better plan for taxes and personal budgeting

- Your limited liability structure remains intact

Step 4: Use accounting software

Accounting isn’t just about tracking — it’s about making informed decisions. Flex plays well with major accounting software like QuickBooks, Xero, and others, allowing you to:

- Sync transactions in real time

- Auto-categorize expenses

- Generate financial reports instantly

- Prepare for tax filing with clean, audit-ready records

Whether you're managing a small team or just getting started, this automation gives you clarity and confidence.

How to Choose the Right Business Banking Setup

The right business banking partner makes separating finances simple and scalable.

Look for:

- No hidden fees or monthly minimums: You shouldn’t be penalized for maintaining a modest balance, especially as a growing business.

- Built-in financial tools: Track expenses, send invoices, and manage cash flow all from one dashboard.

- Mobile-friendly banking: Flexibility is key for entrepreneurs on the go — your bank should work wherever you are.

Why Separate Business and Personal Finances?

Still wondering why it’s important to keep your business and personal finances separate? The answer is simple: it protects you legally, simplifies taxes, enhances credibility, improves operations, and helps build business credit.

Whether you're just launching or scaling your business, taking the time to separate your finances — with the right banking solution — is a crucial investment in your long-term success.

©2025 Flexbase Technologies, Inc., all rights reserved. Flex products may not be available to all customers. See the Flex Terms of Service for details. Terms are subject to change.

Flexbase Technologies, Inc. (Flex) is a financial technology company and is not an FDIC-insured bank. Banking services provided by Thread Bank; Member FDIC.

The Flex Business Credit Card is issued by Lead Bank, pursuant to a license from Visa U.S.A. Inc. and is only available to eligible commercial entities. Fees and terms and conditions apply. Applicants are subject to eligibility requirements.

.png)

.svg)