The Hidden Tax Nobody Talks About

The following article is offered for informational purposes only, and is not intended to provide, and should not be relied on, for legal or financial advice. Please consult your own legal or accounting advisors if you have questions on this topic.

There's a tax that every successful business owner pays. It doesn't show up on a P&L. No accountant tracks it. But it compounds every year, and the more successful you get, the higher it climbs.

It's the coordination tax. And it's paid with time and stress.

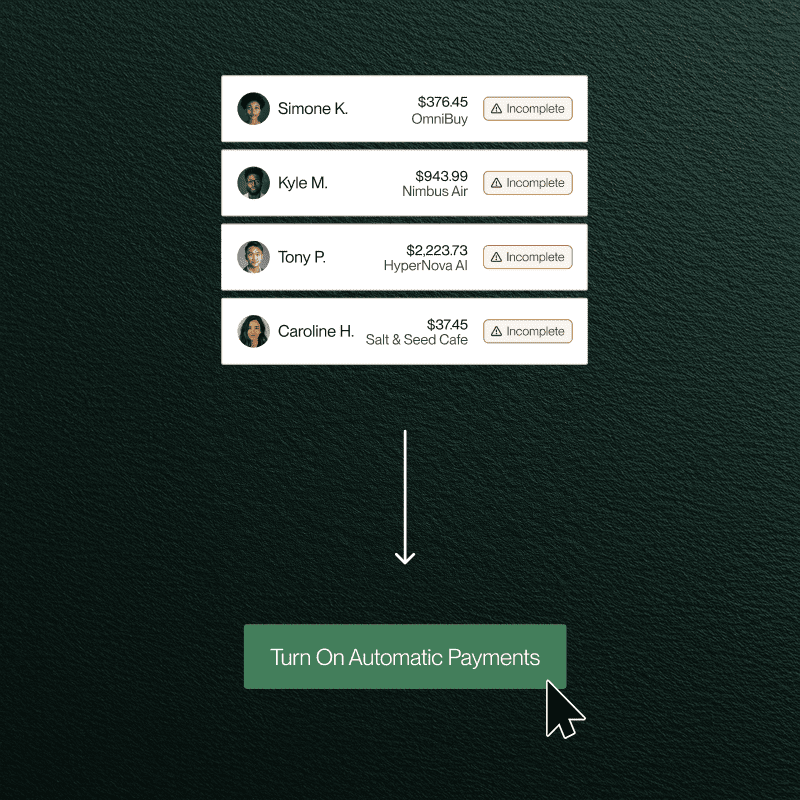

Here's what it looks like. You own a business. And perhaps have it split into a few entities. Each has its own bank accounts, credit lines, vendor relationships, and accounting. Your personal finances are tangled up in all of it. Distributions. Reimbursements. Personal guarantees. Household expenses that cross entity lines.

To manage this, you have a bookkeeper, an accountant (maybe two or five), a wealth manager, a banker or two who don't really understand all of your business, and a credit card company that treats you like every other customer and gives you a coupon book. None of these people talk to each other. You are the integration layer. Your time, your memory, your judgment is the thing holding it all together. And there's usually some incredible employee you rely on that, if they left, would leave you in a terrible situation.

That's the coordination tax. It's invisible. Which is exactly why nobody is solving it.

Why fintech ignores this

This coordination is complex. Very complex. Fintech has been very good at building point solutions. Better bill pay. Faster payments. Smarter expense management. Each product optimizes one narrow slice of a business owner's financial life. These are the easy to see and easy to sell products. They are often just math problems.

The problem is that business owners don't live in narrow slices.

An owner who runs an LLC or two, owns two properties, employs a household staff, and is evaluating an acquisition doesn't need a better expense tool. They need all of their financial infrastructure to be aware of each other. They need their banking to know about their entities. Their credit to understand their cash position across all accounts and underwrite accordingly. Their bill pay to respect their approval policies and controls. Their personal finances to stay connected but appropriately separated from their business.

No one builds this because it's hard. Not just technically hard. Structurally hard. You can't solve coordination by building one great product. You have to build the whole system and make the pieces talk to each other. That means standing up banking, credit, payments, expense management, bill pay, invoicing, treasury, and lending, then connecting them through a shared understanding of the owner's world. Their entities, accounts, people, vendors, policies, and relationships.

That is unglamorous, expensive, and slow. Which is exactly why it's a moat.

The compounding cost

The coordination tax doesn't just waste time. It creates real damage.

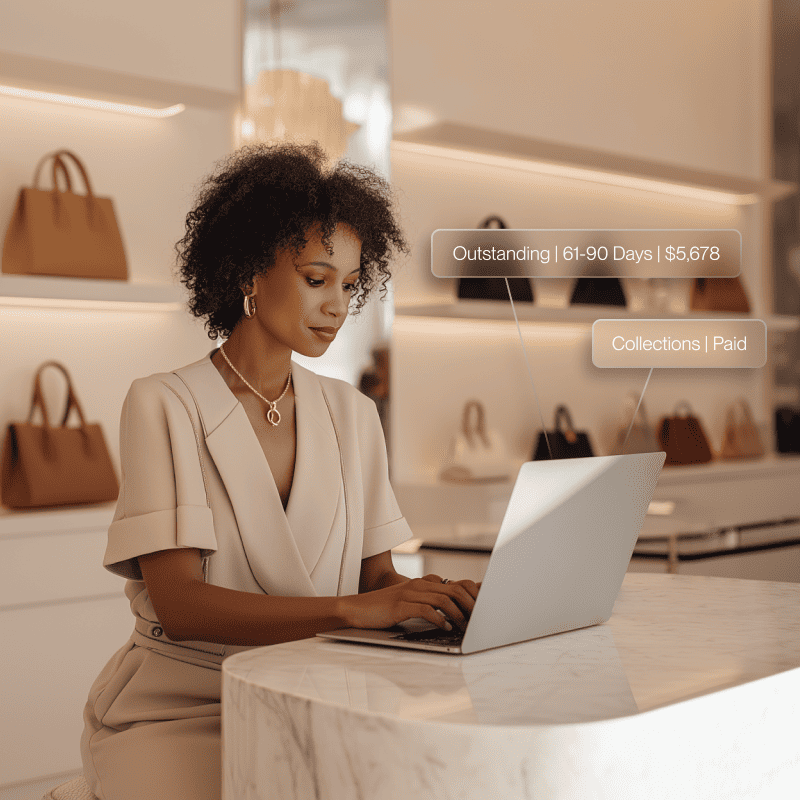

An owner misses a vendor payment because the AP process spans two entities and nobody caught the gap. A distribution gets processed wrong because personal and business accounts don't share context. Month-end close takes three weeks because transactions, invoices, and cards don't agree, and the reconciliation happens in spreadsheets across four systems. End of year taxes are a nightmare with the most important person at a company gathering transaction information and having a call with an accountant.

These aren't edge cases. This is Tuesday for most super premium owners. And the conventional answer, "hire more people," just adds another node to the coordination graph. More email chains, more approval loops, more context that lives in someone's head instead of in the system.

The owners I talk to don't describe this as a coordination problem. They say "I spend too much time on stuff that should be easy." Or "my accountant and I are always out of sync." Or "I need an assistant just to manage my other assistants." They feel it without naming it. And because they can't name it, they can't solve it. They just absorb the tax. They don't even complain about what is really causing them issues because they are conditioned that "it's just part of scaling a company and it's supposed to be hard."

What solving it requires

Solving the coordination problem is not a feature. It's an architecture decision you make on day one and then spend years building toward.

First, you need the financial rails. Real products (banking, credit, payments, cards, bill pay, lending) that work well individually. If the pipes aren't reliable, nothing on top matters.

Second, you need a shared model of the owner's world. Not a dashboard. A model. Entities, accounts, vendors, people, policies, relationships, all connected in a graph that reflects how the owner actually operates. This is the thing that lets one product be aware of what another product is doing. (And even better this is what makes modern AI tooling great as well).

Third, you need a policy and permissions layer that spans everything. The owner sets rules once. Approval thresholds, spending limits, access controls. Those rules apply everywhere. Not per product. Everywhere.

And fourth, once you have the rails, the model, and the policy engine, you've earned something that nobody else can replicate: the data position to make AI genuinely useful. Not "AI-powered insights." Not chatbots. Agents that can perceive the owner's full financial picture, recommend actions, and execute them with the owner's permission. This is the part that gets me out of bed that Flex is creating a new category.

But you only get there if you do the hard work first. The infrastructure earns the intelligence. Skip the infrastructure, and you're building AI on quicksand.

Why now

Two things have changed that make this solvable.

The infrastructure layer in fintech has matured. Issuing cards, moving money, managing ledgers. The primitives are better than they've ever been. Ten years ago, building a multi-product financial platform required massive capital and years of licensing work. Today, the building blocks exist. What's missing is someone willing to assemble them into a coherent system for a specific customer. This still is a long slog. But Flex has done the dirty work for our customers by "simplecting" (our Eng Leads Patrick Flor and Alex Pearson use this word all the time to describe our work) aka hiding the complexity behind our front end so our customers just get incredible experiences.

And AI has reached the point where coordination agents are practical, if they have the right data underneath them. The models are capable. The tooling is real. But capability without context is worthless. You need the unified data model first. Then the AI compounds on it.

This is the window. The infrastructure is available. The AI is ready. The customer is underserved. The only thing standing between the status quo and a fundamentally better experience for business owners is the willingness to do the hard, boring, structural work that makes coordination possible.

That's what we're building at Flex. Not a feature. Not a product. A coordination layer for the financial lives of business owners.

The tax nobody talks about is the one we'll be up every night working to eliminate. And a new category will come from it.

.jpg)

.svg)