Credit Score Ranges: A Breakdown

The following article is offered for informational purposes only, and is not intended to provide, and should not be relied on, for legal or financial advice. Please consult your own legal or accounting advisors if you have questions on this topic.

Your credit score is more than just a number. It’s a key factor that influences your ability to borrow, secure loans, and even negotiate better credit and payment terms. Understanding the different credit score ranges can help you see where you stand today and what steps you can take to unlock greater financial opportunities.

What Are Credit Score Ranges?

When lenders, landlords, or even utility providers evaluate your financial trustworthiness, your credit score is one of the first things they look at. But what exactly are the credit score ranges and what does that mean for you?

In the U.S., most credit scores fall between 300 and 850, based on models like FICO® and VantageScore®. These ranges provide a quick way to gauge how risky or reliable a borrower may be. The higher your score, the better your access to credit, loans, and favorable interest rates.

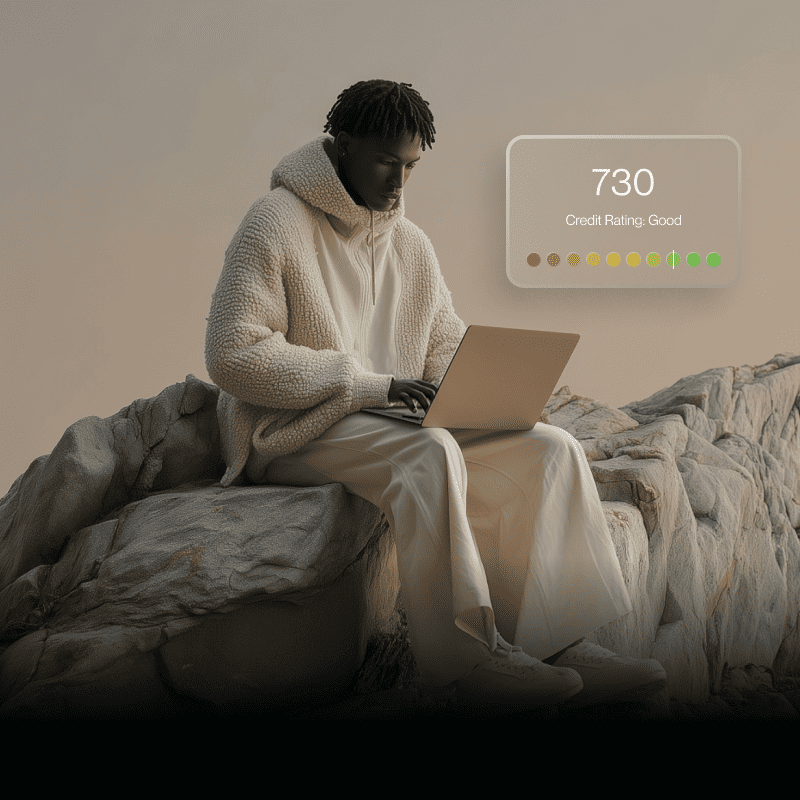

Credit Score Range Chart

To understand where you stand, here’s a credit score range chart that outlines the general categories most lenders use:

How Are Credit Scores Determined?

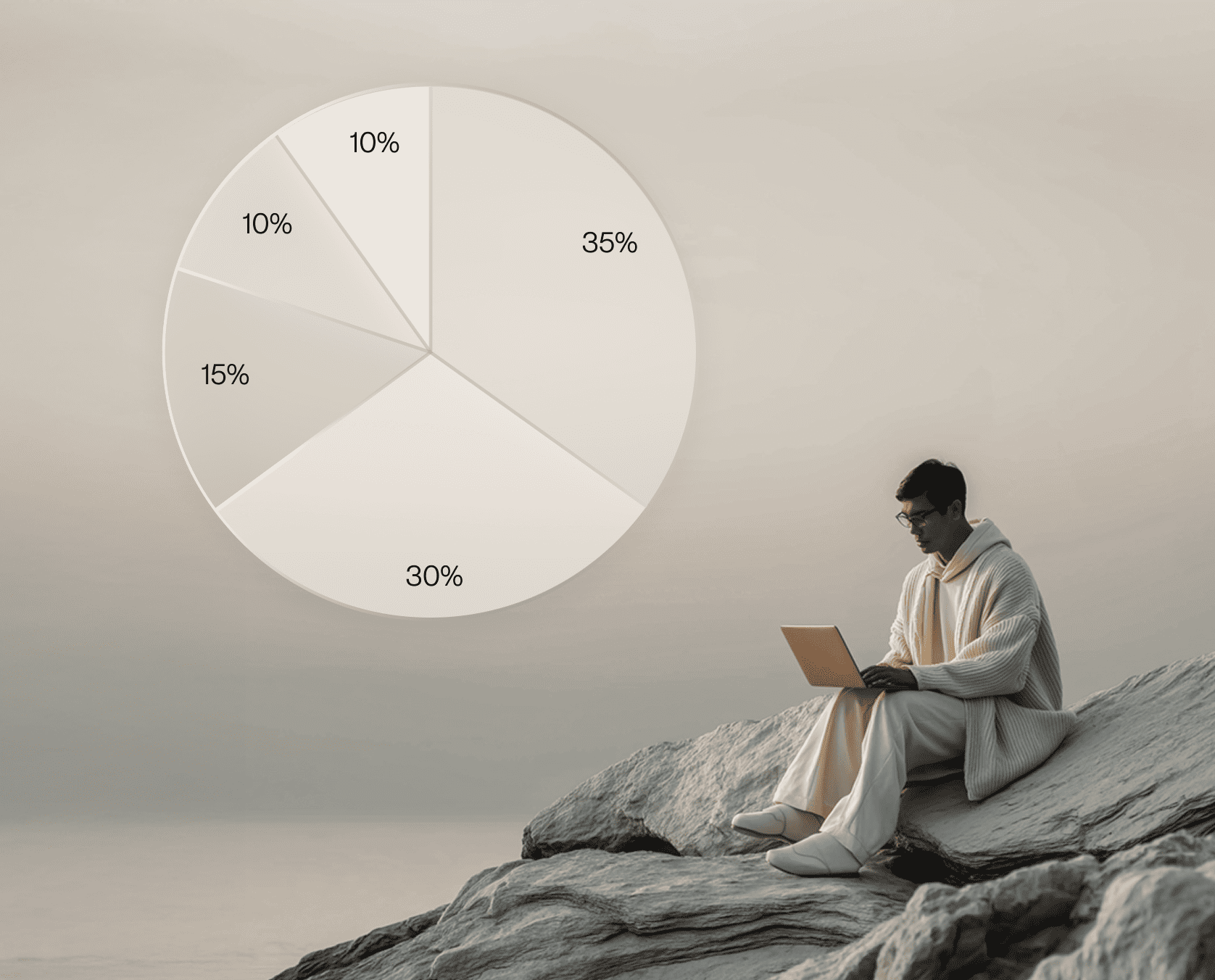

While the exact formula depends on the scoring model, the main factors include:

- Payment history (35%): On-time payments are the single biggest factor.

- Credit utilization (30%): The percentage of available credit you’re using.

- Length of credit history (15%): Older accounts help build credibility.

- Credit mix (10%): A healthy mix of revolving credit (like cards) and installment loans.

- New credit inquiries (10%): Too many applications in a short time can lower your score.

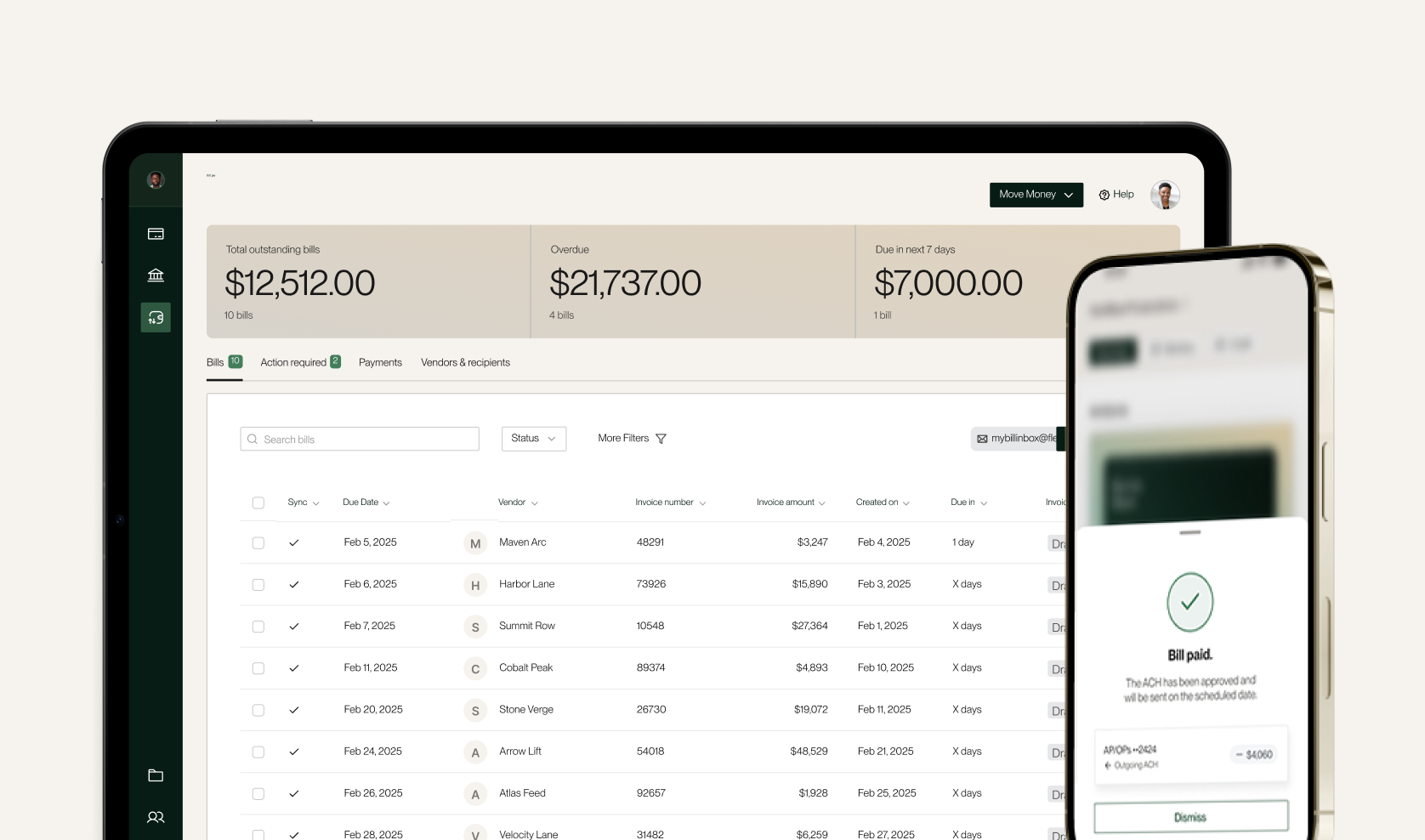

Flex tools, like the Flex Credit Card with extended float and bill pay platform, can help users responsibly manage payments and utilization — two of the most important factors in your credit score. For example, using Flex to pay vendors and then leveraging the float period can give businesses extra breathing room without missing due dates.

What You Can Do at Each Credit Score Range

Depending on where you fall on the spectrum, your strategy for improvement will look different:

Poor (300–579)

- Focus on paying all bills on time.

- Keep credit card balances low or pay them off.

- Consider secured cards or credit-building tools.

Fair (580–669)

- Limit new credit applications.

- Build a more positive history with consistent payments.

- Monitor your report for errors.

Good (670–739)

- You’re in the good credit score range, which opens access to better rates.

- Keep utilization under 30%.

- Use tools like Flex’s invoicing and bill pay features to maintain consistent on-time payments.

Very Good (740–799)

- Shop around for loans or credit cards with competitive interest rates.

- Maintain diverse types of credit responsibly.

- Leverage your score for negotiating power.

Excellent (800–850)

- Maximize buying power with premium products and the lowest interest rates.

- Continue practicing excellent financial habits.

- Take advantage of rewards cards and financial tools like Flex to optimize cash flow.

How Your Credit Score Impacts Buying Power

Your score doesn’t just impact whether you’re approved. It can directly affect how much you’ll pay over time. For example:

- Mortgages: A borrower with a 780 score may secure an interest rate that saves them thousands over the life of the loan compared to someone with a 650 score.

- Business credit: With a higher score, entrepreneurs can access larger credit lines and better payment terms, making it easier to scale operations.

- Everyday expenses: Even your cell phone plan or apartment lease can hinge on your score.

Flex helps level the playing field by giving businesses access to flexible credit lines and extended payment terms, even while they’re working toward higher credit scores. This way, companies can invest in growth without waiting years.

Tips for Improving Your Credit Score

It’s important to remember, improving your score is a marathon, not a sprint. Here are actionable steps:

- Pay bills on time with reminders or automated payments.

- Reduce balances and keep utilization below 30%.

- Don’t close old accounts unnecessarily.

- Review your credit report regularly for errors.

- Use tools like Flex’s bill pay to stay organized and prevent missed payments.

Final Thoughts

Understanding the credit score ranges is the first step to taking control of your financial journey. Whether you’re in the “poor” category or striving to maintain an “excellent” score, the habits you build today shape your access to credit tomorrow.

With Flex, you don’t have to wait until your score is perfect to unlock opportunities. By using products like Flex’s credit card with extended float and automated bill pay, you can stay consistent with payments, manage cash flow effectively, and steadily improve your credit over time.

Flexbase Technologies, Inc. (Flex) is a financial technology company and is not a bank. The Flex Business Credit Card is issued by Lead Bank, pursuant to a license from Visa U.S.A. Inc. and is only available to eligible commercial entities. Fees and terms and conditions apply. Applicants are subject to eligibility requirements.

Bill Pay Later is a product of Flexbase Technologies, Inc. and is subject to eligibility and approval. Availability may vary by state, and not all applicants will qualify. Program limits are determined at approval and may vary by customer.

.png)

.png)

.svg)